Last week, the Social Security Administration (SSA) announced that retirees would be getting an 8.7% cost-of-living raise in 2023. The adjustment is expected to raise Social Security benefit checks by an average of $146 per month, which is a welcome boost for retirees and disabled Americans who are struggling to cover fast-rising housing and food costs.

What is the Social Security cost-of-living adjustment?

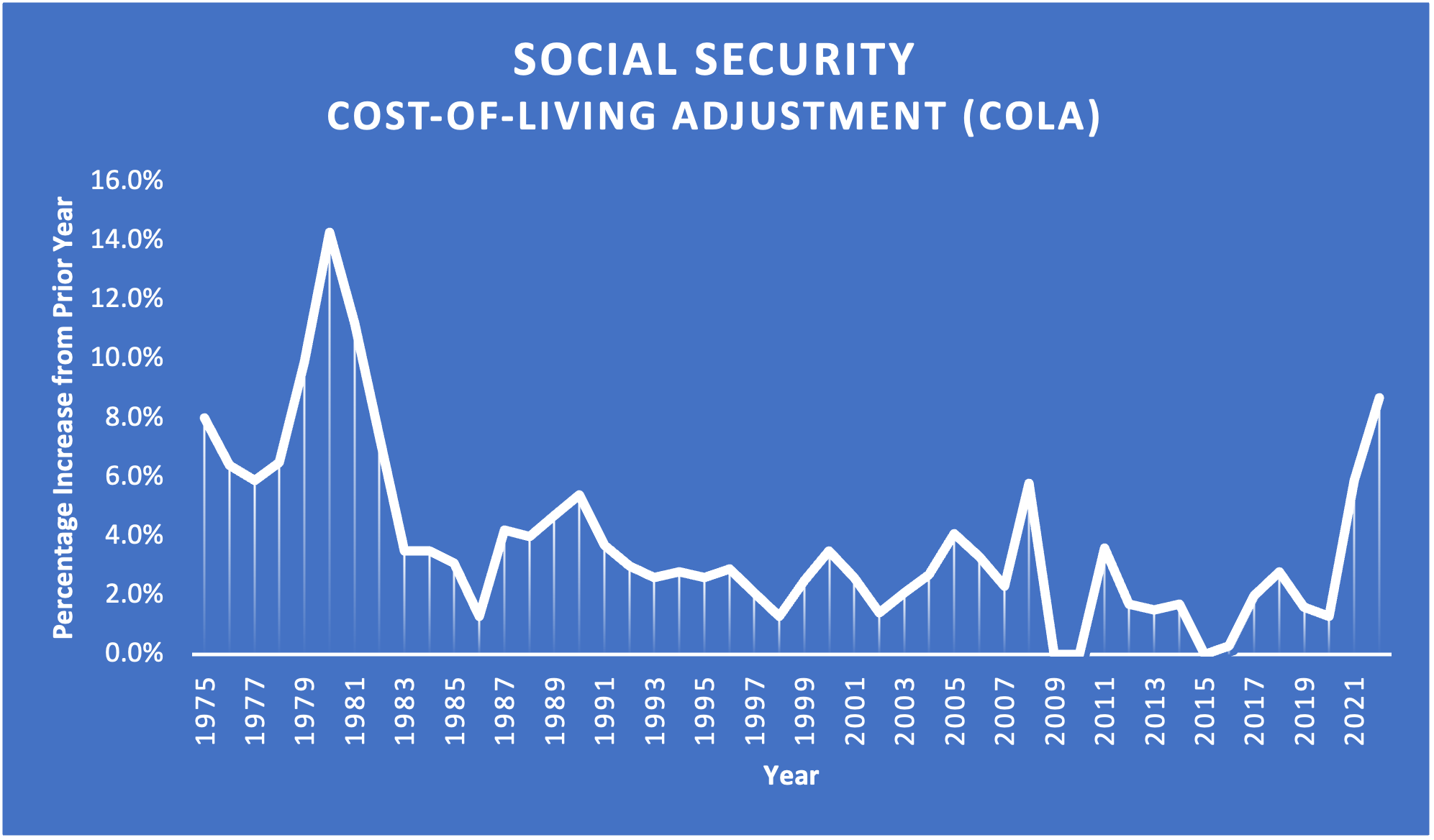

Social Security is adjusted annually for inflation and other economic price increases. The cost-of-living adjustment (COLA) for 2022 is an 8.7% increase from 2021, which is the largest adjustment since 1981. Average COLAs since 1975 have been only 3.8%, making this year’s jump one for the record books.

Source: Social Security Administration

When will the adjustment kick in?

The new cost-of-living adjustment will be applied to benefits beginning in January 2023.

How much will my monthly payment change?

The COLA will raise an average retiree’s benefits by $146 per month, from approximately $1,681 to $1,827. The SSA has released a Fact Sheet that estimates how this will affect different groups of Americans, but you can see your new benefit amount by logging into your my Social Security account.

How often is Social Security adjusted for inflation?

Social Security benefits have been adjusted for inflation every year since 1975. The COLA is announced in the fall based on economic information from the prior 12 months. Although there is some debate about whether the COLA accurately reflects the changes in seniors’ living costs, its purpose is to keep benefits steady as prices increase.

How is the COLA calculated?

The COLA is based on the change in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the third quarter of one year to the third quarter of the next. The average CPI-W for July, August, and September 2021 increased by 8.7% compared to the average CPI-W for the same period in 2022.

Will the COLA affect my tax return?

Nearly all Americans will owe taxes on at least a portion of their Social Security benefits. For example, if you file a joint return with your spouse, you will owe taxes on up to 50% of your benefits if your combined gross income is at least $32,000, and you will owe taxes on up to 85% of your benefits if your combined gross income is at least $44,000. If the COLA increases your combined gross income above these thresholds, you may owe more taxes as a result.

There are a few ways you can reduce or eliminate your current year taxes on Social Security benefits, but these techniques will impact your future tax positions, as well. Before you attempt any new tax strategy, reach out to a CPA who can look at your long-term tax position. They will be able to help you minimize taxes over your lifetime, not just in the current year.

Does COLA affect Medicare premiums?

No, COLA does not affect Medicare premiums, but enrollees in Medicare Part B and those with a Part D prescription drug plan will see an additional increase to their Social Security checks thanks to an unrelated reduction in premiums costs.

Average monthly Medicare Part B premiums will decrease from $171.10 to $164.90, and the average premium for a basic Medicare Part D prescription drug plan will fall from $32.08 to $31.50 starting in January. Since these premiums are deducted from benefits checks, enrollees in Medicare Part B or Part D prescription plans will see an additional increase to their benefits checks.

I’ve chosen to delay my benefits. Will the COLA affect my future Social Security?

If you are eligible for Social Security but have delayed your claim to receive a higher monthly benefit in the future, don’t worry; you’ll still benefit from the COLA. The COLA increases your benefits the year you become eligible for Social Security whether you begin accepting benefits that year or choose to delay them.

Social Security is an essential benefit for many Americans.

Up to 15% of retirees rely on Social Security to cover all or nearly all their living costs. With any luck, these boosted benefits will help those who are struggling to keep up with the price hikes we’ve seen in food and housing costs this year. If you want to discuss how this change will affect your tax plans for 2023, schedule a time to meet with one of our CPAs. We’d love to hear your thoughts on the COLA and discover ways you can improve your tax position in 2023 and years down the road.