In May 2019, Uber posted a $1 billion loss shortly after going public at a valuation of over $80 billion. Several other prominent technology companies are also famed for being loss generating, including Tesla, Airbnb, and Spotify, to name a few.

In May 2019, Uber posted a $1 billion loss shortly after going public at a valuation of over $80 billion. Several other prominent technology companies are also famed for being loss generating, including Tesla, Airbnb, and Spotify, to name a few.

It’s not only Silicon Valley giants that generate a loss and continue to operate. There are nearly 31 million small businesses (less than 500 employees) in the U.S., which accounts for 99.9% of all U.S. businesses. According to a small business statistics study conducted in 2019, approximately 40% of small businesses are profitable, approximately 30% break even, and approximately 30% are continually losing money. To add to the statistics, the devastating impacts of the COVID-19 pandemic have meant that businesses that may have previously been profitable are now struggling to stay afloat.

We are often asked whether a business that does not produce a profit can have a compensable business interruption loss claim. The answer is absolutely. However, there certainly can be instances where a business operates at such a loss that a suspension of the operation is actually economically beneficial, and thus, there is no business interruption loss. Just like nearly everything in business interruption, there is no one size fits all answer, and it comes down to the variables in play and the numbers.

Understanding Business Interruption Coverage

To address this topic, one must start with a basic understanding of what business interruption coverage (synonymous with business income coverage) is and what it is intended to accomplish. The purpose of the coverage is to indemnify the policyholder for what the operation would have done had there been no interruption as a result of a covered cause of loss, subject to the terms and conditions of the insurance policy. In other words, the intention of the coverage is to put the policyholder back into the same economic position they would have been in but for the loss event.

Business interruption, or business income, coverage is defined differently in policies; however, the general intention is the same. For example, the Insurance Services Office’s (ISO) CP 00 30 Form, found in the majority of small- to middle-market risk policies, defines business income as the net income (net profit or loss before income taxes) that would have been earned; and continuing normal operating expenses incurred, including payroll. In the industry, we call this the “bottom-up” approach to measure the business interruption loss, as the wording starts at the bottom of a profit and loss statement (net income or loss) and adds continuing normal operating expenses incurred during the measurement period. Sounds easy, right? Well, one needs to analyze and decipher how to arrive at the projected net income or loss that “would have been earned” and then needs to add continuing “normal” operating expenses. Much easier on paper than in practice.

In the middle-to-larger risk space, you will often find customized, or manuscript, policies that include gross earnings language for business interruption. In simple terms, the language defines the business interruption coverage as lost revenue less non-continuing expenses. In the industry, we call this the “top-down” approach to measure the business interruption loss, as the wording starts at the top of a profit and loss statement (revenue) and deducts non-continuing expenses (a.k.a. saved expenses).

To us forensic accountants, this approach is by far easier to explain to those with limited experience with business interruption, as it is more logical, and thus, easier to digest. The simple thought that a business loses revenue and saves some expenses as a result when operations are partially or totally suspended tends to be more palatable when first approaching the measurement. However, again, much easier on paper than in practice.

Are you ready for the kicker? It does not matter if the coverage is written “bottom-up” or “top-down.” When approached properly, both approaches arrive at the same loss value. We utilize a presentation that serves as a hybrid, demonstrating both the “bottom-up” and “top-down” presentations at the same time. It’s called the “three-column” approach.

Business Interruption Loss Measurement Scenarios

So, let’s get back to the question at hand. Can a business that historically operates in the red (at a loss) have a compensable business interruption loss? Perhaps it’s best to demonstrate my “yes and no” response when this all started with a few exhibits. And, you guessed it – I’m going to present the exhibits with the three-column approach, so you can see both the “bottom-up” and “top-down” approaches.

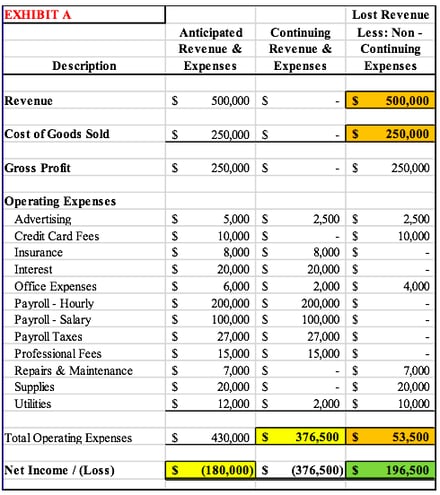

For simplicity, in both exhibits, let’s assume that there are no policy provisions that would impact the measurement (limits, deductibles, waiting period, ordinary payroll limitation or exclusion, etc.). And, let’s assume that XYZ Corporation experienced an insured event, at their sole location, that completely suspended their operation (partial suspensions and multiple locations are much more complex).

In Exhibit A below, note the color-coding. The yellow highlighted figures summarize the “bottom-up” approach, with the orange highlighted figures summarizing the “top-down” approach. The green highlighted figure represents the measured business interruption loss, under both approaches.

In the “bottom-up” approach, we anticipate a net operating loss of $180,000 for this operation. However, the continuing expenses of $376,500 exceed the anticipated net operating loss, yielding a business interruption loss of $196,500. In the “top-down” approach, we measure a $500,000 revenue loss. However, there are $303,500 in total non-continuing expenses ($250,000 + $53,500). The lost revenue less the non-continuing expenses yields the same business interruption loss of $196,500.

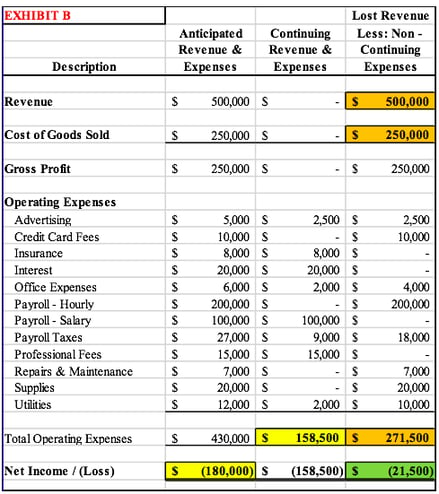

In Exhibit B below, we are going to approach everything the exact same as above. However, the sole tweak in this scenario is the insured (XYZ Corporation) decided to not pay their hourly employees during the loss period. In the “bottom-up” approach, the continuing expenses do not exceed the anticipated net operating loss. And, in the “top-down” approach, the non-continuing expenses exceed the measured lost revenue. In other words, the insured is actually in a better financial position than had the loss event not occurred. Therefore, there is no compensable loss. Importantly, the insured operated at a net loss of $158,500 during the loss period, a position that was better than the projection. Their expenses exceeded their revenue by a lower amount than was anticipated and they lost less money than expected as a result of labor reductions that occurred due to the loss event.

The COVID-19 Factor

It goes without saying that the global pandemic took its toll on businesses throughout the world, especially small businesses. As of December 2020, nearly one-third of small businesses in the U.S. were not operational (and over 70% were not operational in March and April 2020).

The COVID-19 impact has created a whole new dimension in the challenges of measuring business interruption losses, not only for insured events that occurred during the pandemic but for insured events that will occur for years to come, as the historical operational performance of businesses has been skewed by an event never seen before (negatively for some and positively for others). Businesses that may have been profitable pre-pandemic may have been highly unprofitable during the pandemic (or vice versa). And, it is to be seen where they go post-pandemic, as there is no question that the world has changed, and the way business is conducted has changed, due to COVID-19.

Business Interruption Is Never Simple

There are always more variables in play than one could imagine. And, more times than not, the answer to a specific inquiry regarding how to measure a business interruption loss contains the words “it depends” somewhere in the response. So, to summarize and answer the question, yes, a business that operates at a deficit could have a compensable business interruption loss. However, it depends.