The PPP program hasn’t changed much recently, other than the application deadline getting extended five more weeks until early August. This has given everyone some more time to start thinking more in depth about their forgiveness applications. One of the most common questions we’ve received from clients and other companies has been what covered period should I use, 8-weeks, 24-weeks, or something in between?

The PPP program hasn’t changed much recently, other than the application deadline getting extended five more weeks until early August. This has given everyone some more time to start thinking more in depth about their forgiveness applications. One of the most common questions we’ve received from clients and other companies has been what covered period should I use, 8-weeks, 24-weeks, or something in between?

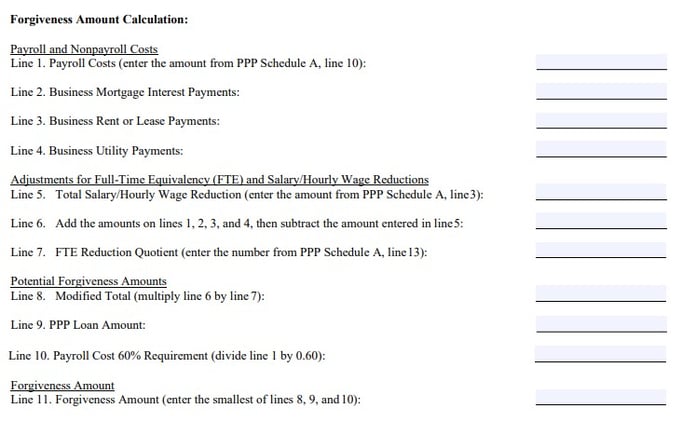

While there are a lot of factors that could impact your decision, as we discussed in an earlier blog here, one major thing to keep in mind is that the FTE and Salary reductions are calculated off your total eligible expenses, which you can see in the snippet of the forgiveness application below. If that amount is higher than your loan total, even after the reductions, then the entire loan would still get forgiven since you choose the lowest number from lines 8 through 10. So, the more expenses you have, the less of an impact any of the reductions will have on you. This would make the case for using a longer covered period. For example, if your loan were $1 million and your 24-week expenses were $3 million, and you had a 50% reduction in employees for whatever reason, you’d still have $1.5 million after the reductions are applied, which is more than the loan total meaning the entire loan is still forgiven. If you only used 8-weeks and had say $1 million of costs (about 1/3rd of the 24-week amount in this example) then the reductions would have a more significant impact on your forgiveness.

This is not a change from the previous version of the application before the law changed to allow up to 24-weeks, but wasn’t really a consideration because with only 8-weeks typically the expense total was lower than the loan amount, so this didn’t apply.

While there are a lot of different factors that could impact your decision on when to apply for forgiveness, if you are concerned about the impact of the FTE and Salary reduction penalties, accumulating more expenses by using a longer covered period may be an option to consider. If you need assistance with trying to determine what might work best for you, please contact us.